Retirement Savings Options

Wondering how much you should save for retirement each month? While most financial experts will tell you to save as much as you can for retirement, the standard is to put away between 10% and 15% of your total income each month. The earlier you start saving, the better off you’ll be, so we recommend starting at age 20 and building up your savings as much as you can over the course of the next 40 to 50 years. By the time you retire, you want a nest egg between $200,000 and $300,000 to bridge the gap between your social security checks and the additional funds you need to pay the bills.

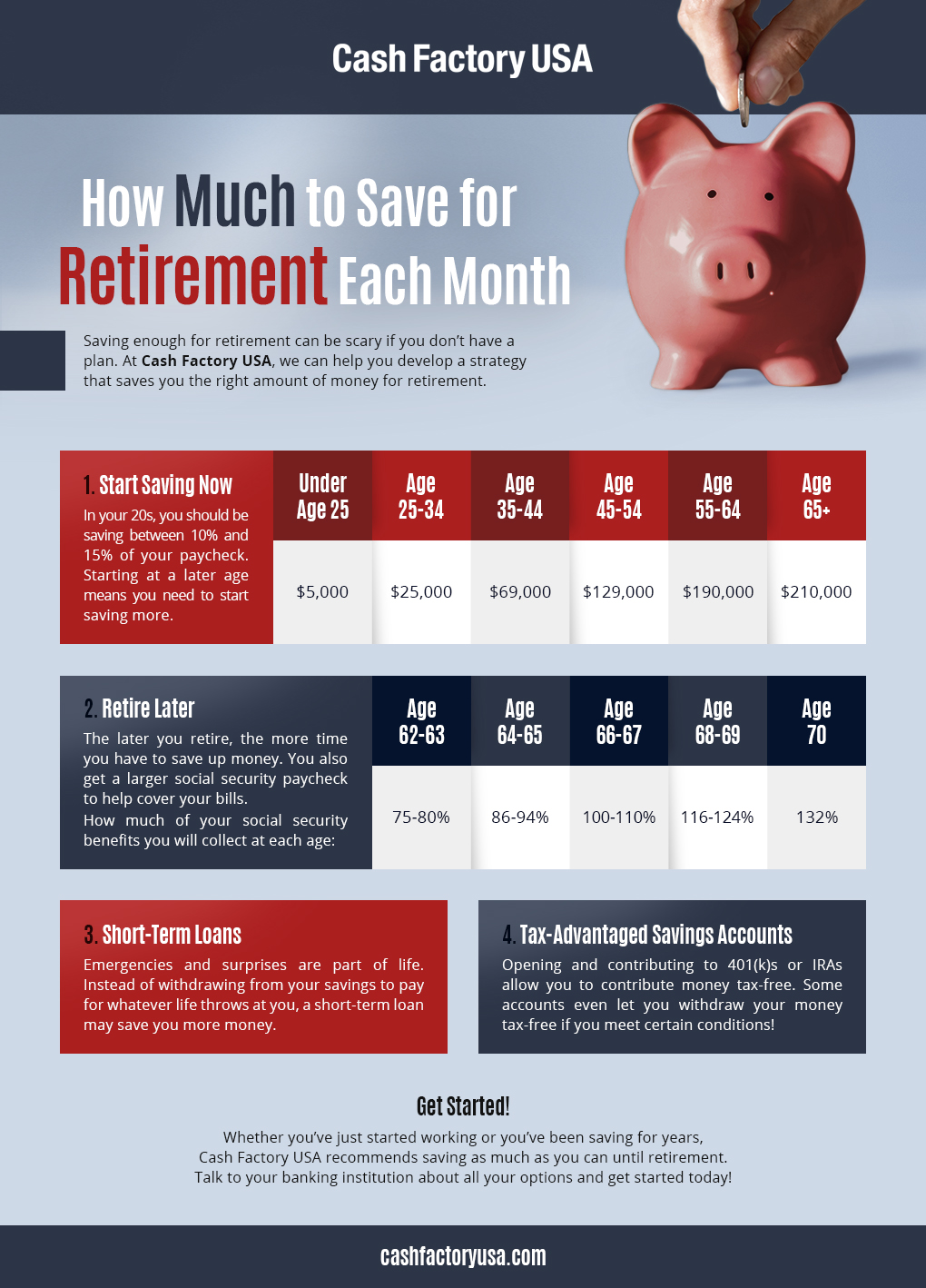

Wondering how to do that? Check out what Cash Factory USA has to say about retirement saving strategies and more.

1. Start Early

As we said earlier, you want to start saving as soon as possible. Even if you’re only making minimum wage, you could be putting away $100 a month. Every dollar makes a difference. If you’re a little more than 20 and you’ve just now started to think about retirement, that’s okay! It’s never too late to start.

Wondering how much you should save for retirement each month? Consider saving more than the standard 10% of your paycheck. Cutting down on eating out, foregoing expensive trips and entertainment will help you save more money over time.

After eight years in the workforce, you want to have $50,000 to $100,000 saved. Every 10 years after, this amount should double to keep up with inflation and ensure you have enough by age 70

2. Delay Retirement

If you follow the 15% rule to answer the question how much you should save for retirement each month, you’re assuming that you’ll retire at age 67. If you decide to delay retirement, you can save less each month, or you can save the same amount for a higher total when you finally do stop working. Delaying retirement also results in higher social security checks each month, so the gap between the bills that social security can cover and what’s left over for you to pay is much smaller.

3. Consider Short-Term Loans

While your checking account doesn’t pay out any interest, your savings accounts do, so you always want to make sure that the bulk of your money is there. If you’re stuck in a bind and you need extra money to pay for surprise repairs or emergency situations, consider a short-term loan. At times, the interest on a loan is smaller than the amount you’re getting back in a savings account, so choosing a loan instead of paying out from your savings ends up netting you more money at the end of the day.

4. Look Into Tax-Advantaged Savings Accounts

You’ll want to save more than the standard 15% if you’re starting at an older age or you want to save as much as possible. Once you’ve figured out how much you should save for retirement each month to ensure a big enough safety net, you can investigate tax-advantaged savings accounts.

Ask your bank about 401(k)s and IRAs where you can contribute money to reduce your taxable income. Anything you place in these accounts isn’t taxed at the end of the year! This money can grow tax-free until you start withdrawing it, at which point it is taxed as income. Fortunately, there are some savings accounts that allow you to withdraw tax-free as long as you meet certain conditions.

Start Saving!

Hopefully, we’ve given you a solid overview of how much you should save for retirement each month and explored some of the most popular retirement savings options for you. Now it’s time to start saving!

Have questions about short or long-term loans? Reach out to our team today for more information!