There has been a pattern of rising interest rates from the Federal Reserve over the past few years that affects the finances and credit of millions of Americans. If you have a home mortgage, student loan, or car loan, these interest rate increases have effects on your life too — even if you don’t borrow money directly from the government.

But what does it really mean when there is an increase in interest rates in the Federal Reserve? Learn more about the real cost of higher interest rates with help from Cash Factory USA.

More Expensive Loans

Increased interest rates almost always result in more expensive loans for any bank that is borrowing from the Federal Reserve. Instead of taking the brunt of the cost on themselves, banks pass on the costs to customers. They raise the rates for loans for everyone! Unfortunately, any customers that have subpar credit are impacted much more, because their base interest rates are already much higher than those people with acceptable credit scores.

In addition to rising interest rates from banks, you can also expect credit card companies to increase their own interest rates, minimum monthly payment amounts, and even late fees.

Less Disposable Income

Since you’re now paying that much more money on your loans than before, you suddenly have less money left at the end of each month to spend on groceries and other necessities. Since your mortgage, student loans, and car payments are among the priority bills to go out each month, you need to keep an eye on your other finances. Tighten your budget and try to minimize the use of your credit cards in order to avoid spending extra money on interest.

Easier to Get a Loan

Since loans suddenly become more expensive because of increased interest rates, fewer people approach banks to apply. In order to ensure they’re still giving out a large volume of loans (because remember, banks make money off of loans), banks make it slightly easier for the average American to get approved. An effect of interest rate increases may be that banks take on riskier loan approvals for those with poor credit.

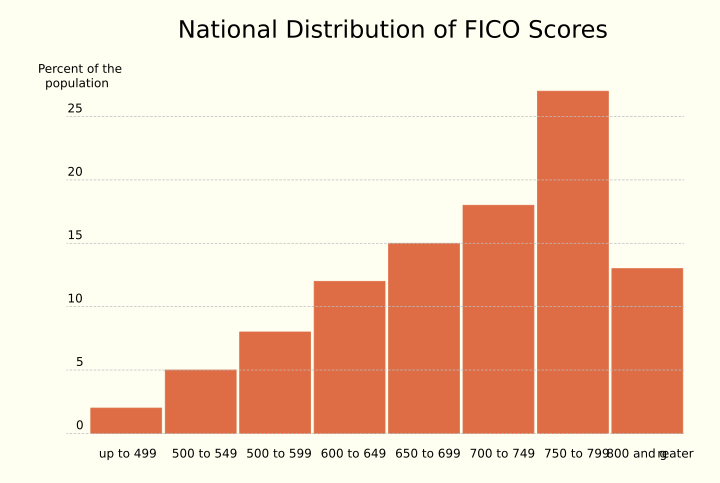

Lower Credit Scores

If you carry a balance on your credit card from month to month, an increased interest rate means you owe more than you did before — even if the amount you spent is the same. Due to higher costs, you may be using more of your available balance and end up with a higher utilization ratio. Since you want to use less than 30% of your total credit limit to maintain a higher credit score, your score could go down if you don’t pay enough of your balance each month!

Because the Federal Reserve raised its rates to 1.75% in 2018, credit card companies are following suit. Your credit card company must give you a 45 day notification before raising rates, giving you enough time to change cards, close accounts, or transfer balances.

General Effects

Personal finances aren’t the only ones impacted by increased interest rates. Businesses who would have taken out a loan to expand may decide not to, curbing their growth and advancement. With less spending money for the individual and lower growth rates among businesses, the economy in general suffers each time the rates go up.

If you’re finding that you need a little more money at the end of each month to make ends meet because of rising interest rates, explore your options with payday loans or installment loans from Cash Factory USA.